Think You Need 20% Down To Buy in Lathrop? Most First-Time Buyers Don’t

Think You Need 20% Down To Buy in Lathrop? Most First-Time Buyers Don’t

By David Torres | Broker Associate, Real Broker

After a weekend of showing homes in Lathrop, one conversation tends to come up again and again with first-time buyers.

They like the idea of owning.

They are watching the market.

They may even be browsing homes for sale in River Islands Lathrop late at night.

But then the same concern comes out:

“We probably need 20% down first, right?”

That belief has stopped a lot of would-be buyers from taking the next step. Not because they are unqualified. Not because they are not serious. But because they are working off an old assumption that simply does not reflect how many buyers purchase homes today.

And that matters, especially here in Lathrop, where buyers are trying to balance rising living costs, changing mortgage rates, and the desire to plant roots in a community that continues to grow.

The truth is, most first-time homebuyers do not put 20% down.

That does not mean 20% is bad. In some situations, it can be a strong move. But it is not the baseline requirement many people think it is. And if you have been waiting until you hit that number before even exploring your options, you may be stretching your timeline longer than necessary.

Many first-time buyers are not priced out. They are simply misinformed about what it takes to get in.

Why So Many Buyers Still Believe the 20% Down Myth

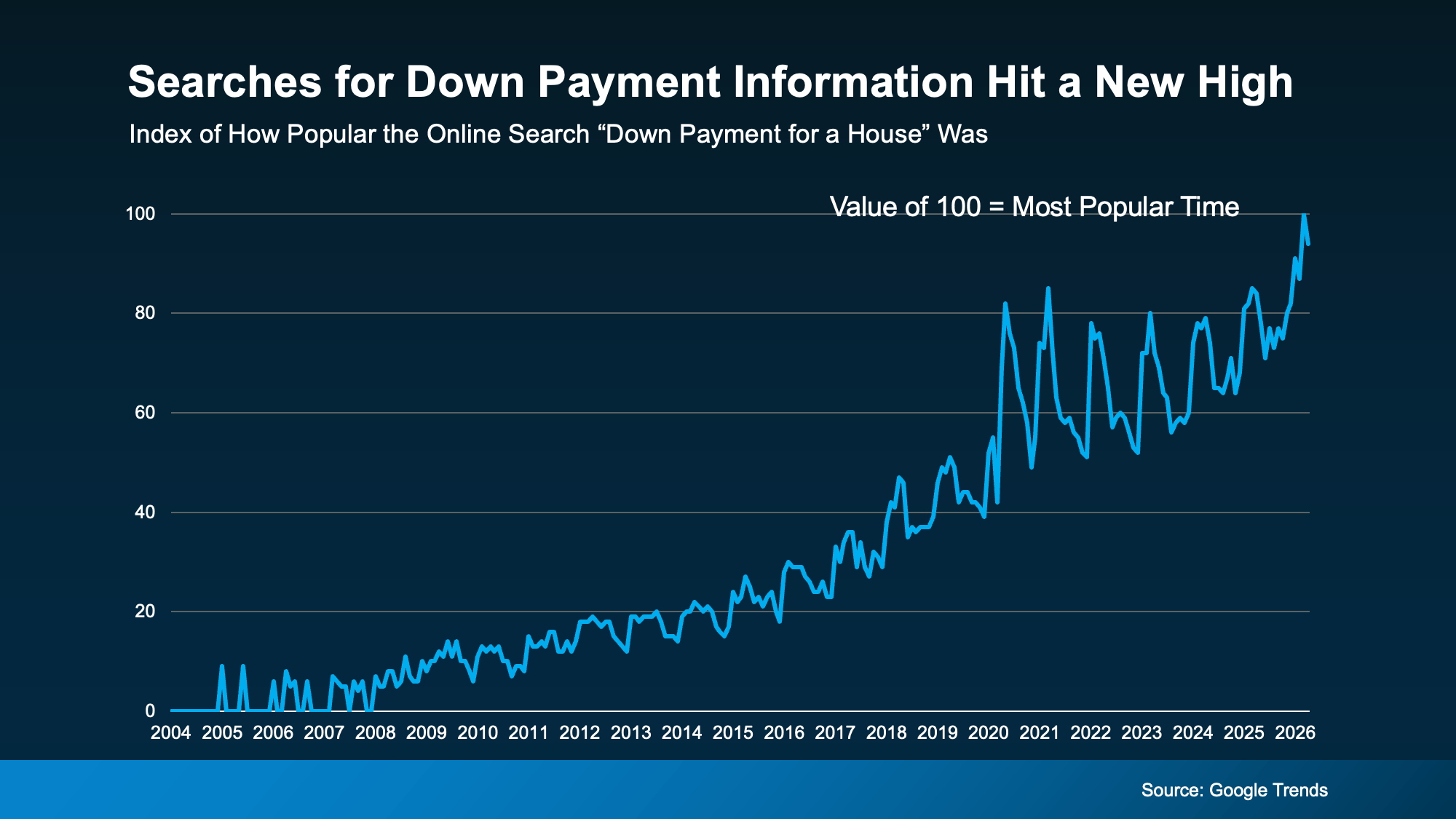

According to Google Trends, online searches related to down payment information recently hit an all-time high. That tells us one thing very clearly: buyers are actively trying to understand what they really need to save before buying a home.

That makes sense.

When someone starts thinking about buying, one of the first questions is usually about money. How much do I need? What will my monthly payment look like? How much cash should I have set aside before I even talk to a lender?

And somewhere along the way, a lot of people hear the same message: you need 20% down.

That idea has been around for years, and it is one of the most persistent myths in real estate.

Yes, there can be benefits to putting 20% down. Depending on the loan, it may help reduce certain costs, improve loan terms, or eliminate mortgage insurance in some cases. But that is very different from saying it is required in every scenario.

For many first-time buyers, it is not.

Unless a lender specifically tells you otherwise, a 20% down payment is typically not mandatory. In fact, there are loan options designed specifically to help buyers get into a home with much less upfront.

As The Mortgage Reports explains, the amount you need to put down depends on factors like your loan type and your financial goals. If you do not have a large down payment saved, there are still options available, and some buyers are able to purchase with as little as 3% down or even no down payment at all.

That is a major shift from what many people assume.

What Loan Options Can Make Buying Possible With Less Down?

This is where local guidance matters.

A buyer searching online may see national advice, broad estimates, or generic financial tips. But real strategy starts when you sit down with a trusted lender who can tell you what actually applies to your situation.

Several common loan types allow lower down payments than many buyers expect:

FHA loans

FHA loans can allow down payments as low as 3.5% for qualified buyers.

VA loans

VA loans can offer zero down payment options for qualified Veterans and eligible borrowers.

USDA loans

USDA loans may also offer zero down payment options for qualified buyers in eligible areas.

The right fit depends on income, credit profile, military status, location, and the property itself. That is why no serious buyer should rule themselves out based on a blanket assumption.

In a market like Lathrop, where buyers may be comparing newer homes, resale homes, and opportunities in areas like River Islands, having access to multiple financing paths matters.

The goal is not to guess your way into homeownership. The goal is to know your real options.

What Are First-Time Buyers Actually Putting Down?

If first-time buyers are not typically putting down 20%, what are they doing instead?

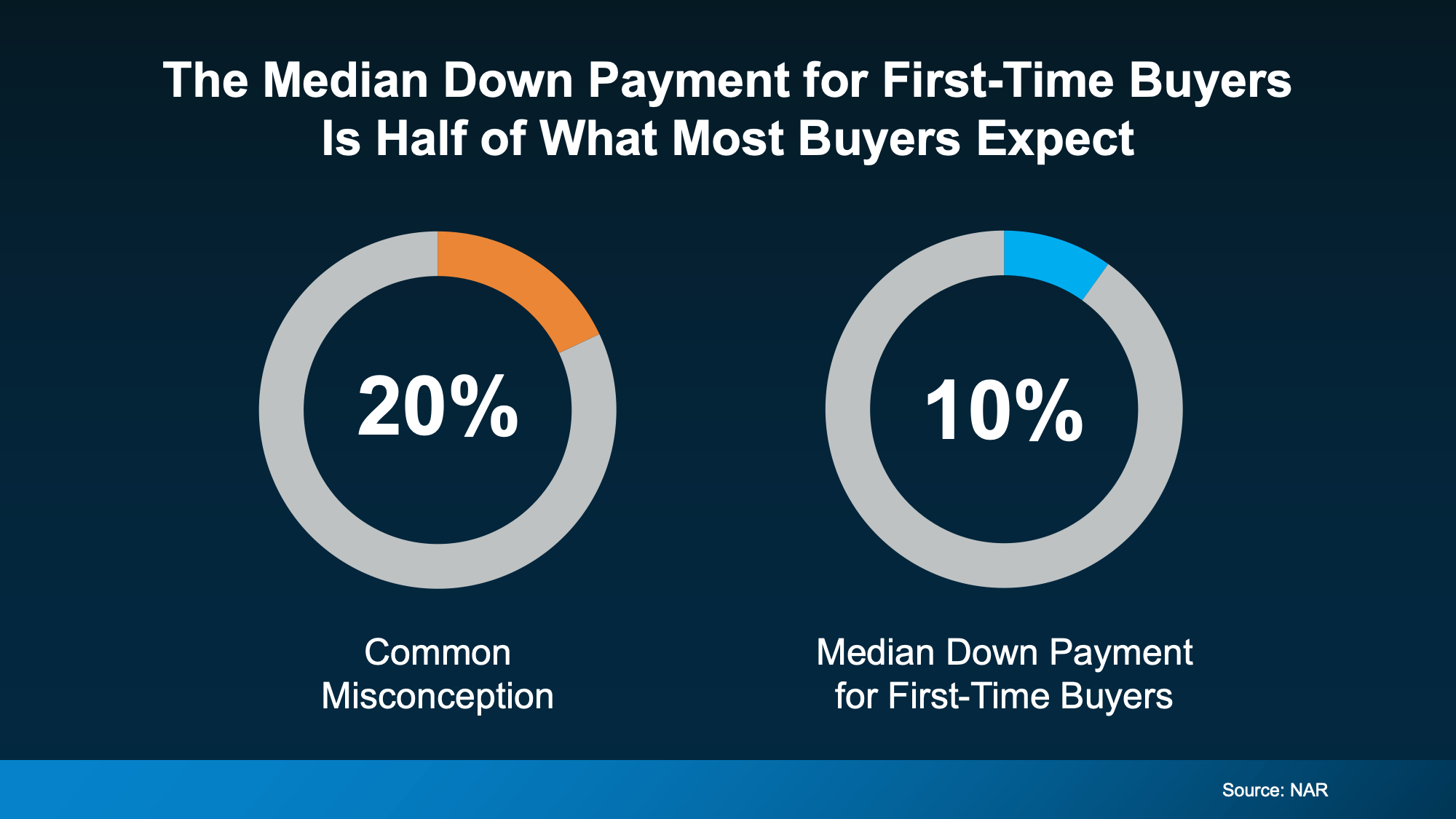

According to the National Association of Realtors, the median down payment for first-time homebuyers is 10%.

That is half of the number many people assume they need.

This is one of the most important takeaways in the entire conversation because it changes the timeline buyers build in their head.

If someone thinks they must save 20%, they may decide they are still years away from buying. That belief can cause them to delay conversations with lenders, avoid looking at homes, and miss opportunities they may already be closer to than they realize.

But if the actual median for first-time buyers is 10%, the picture changes.

That does not automatically mean 10% is your number. Your required amount could be lower or higher depending on your loan and qualifications. The point is that many buyers are aiming for a target that is larger than what the market actually shows most first-time buyers use.

And when that happens, waiting can become a habit.

In real estate, that matters.

Because while someone is waiting to hit an assumed 20% mark, they may also be watching home prices, interest rates, and inventory shift around them.

Why This Matters for Buyers in Lathrop and River Islands

For buyers looking at homes for sale in River Islands Lathrop or elsewhere in the city, affordability is not just about the purchase price. It is about the full strategy.

That includes:

- how much cash you truly need upfront

- what loan programs may fit your situation

- whether you qualify for assistance

- what monthly payment works for your lifestyle

- how quickly you want to move

- whether buying now makes more sense than continuing to wait

In communities like River Islands, many buyers are drawn in by the lifestyle, newer homes, schools, amenities, and long-term appeal. But even when the interest is strong, confusion around down payments can keep people from taking a serious first step.

That is why this topic matters so much.

You do not need perfect knowledge before you begin. But you do need accurate knowledge.

The difference between those two is often what moves someone from “maybe someday” to “we are actually doing this.”

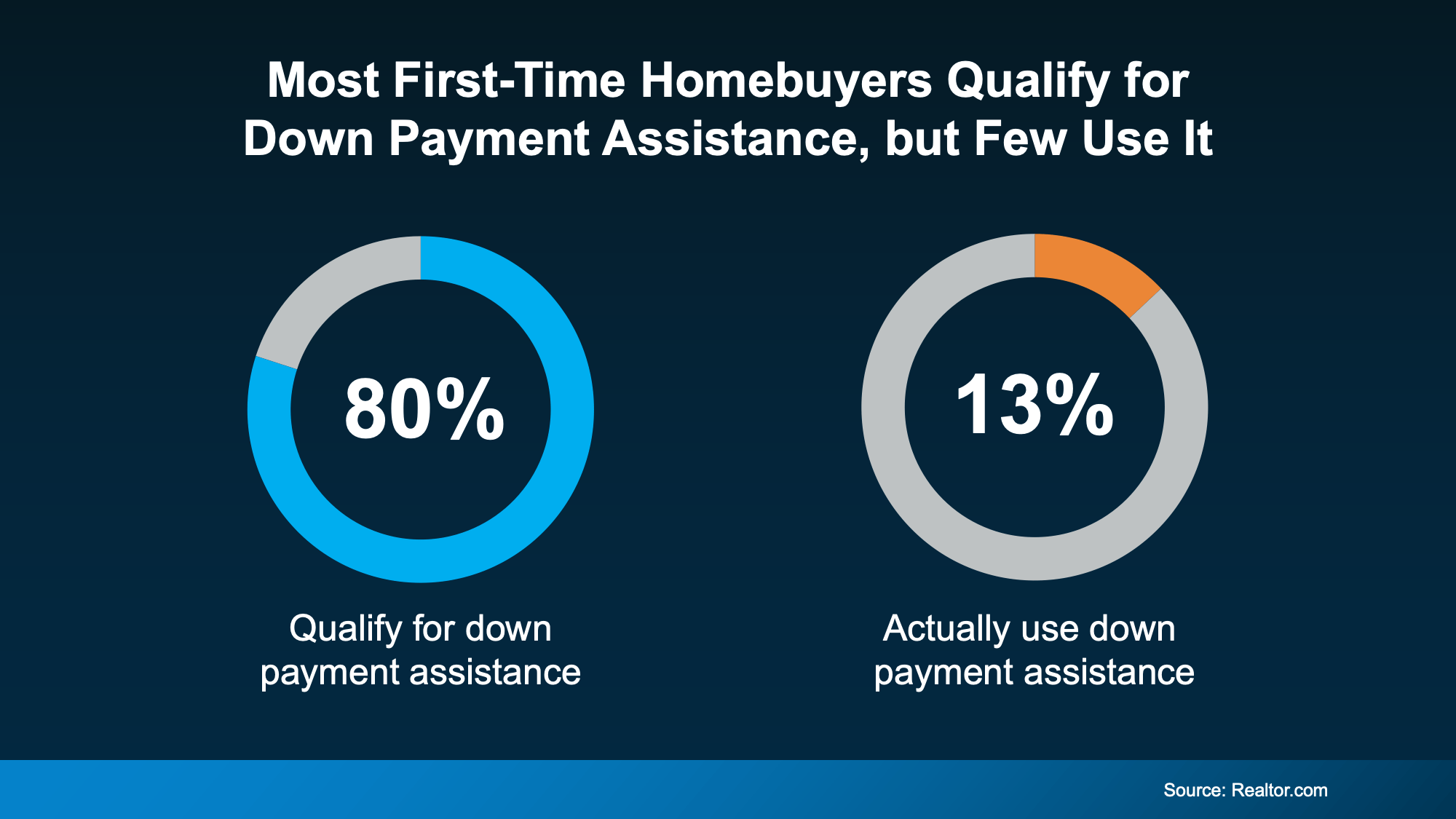

Why Down Payment Assistance Programs Deserve More Attention

There is another part of this conversation that does not get enough attention.

Even buyers who know they may not need 20% down often assume they are completely on their own when it comes to coming up with the money they do need.

That is not always true.

There are many down payment assistance programs designed to help buyers bridge the gap, and they can make a meaningful difference.

Research from Realtor.com shows that almost 80% of first-time homebuyers qualify for down payment assistance, but only 13% actually use it.

That gap is huge.

It means many buyers who may be eligible for help either:

- do not know these programs exist

- assume they will not qualify

- never ask the right questions early enough

And that can keep them stuck longer than necessary.

According to Down Payment Resource, there are more than 2,600 homeownership programs available in the U.S., and the average benefit is $18,000.

That is not a small number.

An extra $18,000 can materially change what a buyer is able to do. It can help with:

- the down payment

- upfront costs

- reducing the savings burden

- getting into the market faster than expected

In some situations, buyers may even be able to stack multiple programs, creating an even stronger financial advantage.

Sometimes the gap between renting and owning is not 20%. It is access to the right information.

Could You Qualify for Down Payment Assistance?

This is the type of question buyers are already asking search engines and voice assistants, so it deserves a direct answer.

Who qualifies for down payment assistance?

Many first-time homebuyers may qualify for down payment assistance, but eligibility depends on factors like income, loan type, location, military status, and whether the program is designed for specific buyer groups such as first-generation or repeat buyers. Since Realtor.com reports that nearly 80% of first-time buyers may qualify, it is worth asking a trusted lender what programs may apply to your situation before assuming you are not eligible.

That answer is simple, direct, and important.

Too many buyers assume assistance is only for one narrow type of borrower. But programs continue to expand and serve a broader range of incomes, property types, and borrower needs, including first-generation buyers, military buyers, and even some repeat buyers.

That does not mean everyone qualifies. It does mean more people should look into it than currently do.

Should You Wait Until You Save More?

This is where buyers often get stuck.

Waiting can feel responsible. In some cases, it is the right move. If someone needs more time to improve credit, build reserves, stabilize income, or reduce debt, patience can absolutely be a smart strategy.

But waiting based on a myth is different from waiting based on a plan.

If you are delaying your purchase only because you assume you need 20% down, there is a good chance your timeline is being shaped by bad information.

A better approach is to replace assumptions with specifics.

Ask:

- What loan options are available to me?

- What is the minimum down payment for my situation?

- Are there any assistance programs I may qualify for?

- What monthly payment range makes sense for me?

- If I want to buy in Lathrop or River Islands, what should I be preparing now?

Those are productive questions.

They move you toward a real answer instead of keeping you parked in uncertainty.

What First-Time Buyers in Lathrop Should Do Next

If you are thinking about buying your first home in Lathrop, River Islands, or the surrounding area, here is the move I would recommend.

Do not start with the assumption that you need 20% down.

Start with a conversation.

Talk to a trusted lender who can review your numbers, explain your financing options, and help you understand what is realistic based on your goals. That one conversation may save you months or even years of unnecessary waiting.

And if you are also wondering where to start on the home search side, that is where local expertise matters too.

A buyer looking in Lathrop is not just choosing a price point. They are choosing:

- neighborhood feel

- commute patterns

- school considerations

- home style

- resale potential

- whether a newer master-planned community like River Islands fits their long-term goals

That is why financing and local strategy should work together.

Bottom Line

Most first-time homebuyers do not put 20% down.

According to the National Association of Realtors, the median down payment for first-time buyers is 10%. FHA loans may allow as little as 3.5% down, and VA and USDA loans can offer zero down payment options for qualified buyers. On top of that, down payment assistance remains one of the most underused tools available, with nearly 80% of first-time buyers potentially qualifying while only 13% use it, and average assistance benefits around $18,000.

If you have been waiting because you thought 20% was the minimum, you may be setting a longer timeline than necessary.

The smarter next step is to find out what you actually need, not what the myth says you need.

If you are thinking about buying in Lathrop, CA or River Islands, connect with a trusted lender and a local real estate expert who can help you understand your real options and map out the right next step.

The path to homeownership may be closer than you think.

FAQ Section

Do you need 20% down to buy a home in Lathrop, CA?

No. Many first-time homebuyers purchase with less than 20% down. The actual amount depends on the loan type, lender requirements, and buyer qualifications.

What is the average down payment for first-time homebuyers?

According to the National Association of Realtors, the median down payment for first-time homebuyers is 10%.

Are there zero-down loan options for first-time buyers?

Yes. VA and USDA loans may offer zero-down options for qualified buyers.

Can FHA buyers purchase with less than 20% down?

Yes. FHA loans may allow qualified buyers to purchase with as little as 3.5% down.

What is down payment assistance?

Down payment assistance refers to programs that help eligible buyers with funds for their down payment or other upfront homebuying costs.

Do many first-time buyers qualify for down payment assistance?

Research from Realtor.com shows nearly 80% of first-time homebuyers may qualify, though only 13% use it.

How much help can down payment assistance provide?

According to Down Payment Resource, the average benefit is $18,000.

Is River Islands a good place for first-time buyers to explore?

For many buyers, yes. River Islands attracts buyers looking for newer homes, community amenities, and a master-planned environment in Lathrop. The right fit depends on budget, lifestyle, and long-term goals.

If you are thinking about buying your first home in Lathrop or River Islands, do not let the 20% down myth keep you on the sidelines longer than necessary.

The best move is to get clear on what is actually possible for you.

I can help you understand the local market, the neighborhoods, and what to look for as you start planning your next step. And I can connect you with trusted local lenders who can break down your financing options and help you see whether buying may be closer than you think.

If you are considering buying in Lathrop or River Islands, reach out and let’s talk through your next move.

Categories

Recent Posts